My dad retired in 2000 with a salary that today would not be able to buy you many dinners in Mumbai. Had he left his money in the bank without investing it in mutual funds, stocks and fixed deposits, we would have struggled to be where we are today as a family. Moreover, my sister and I would NOT have got quality education that we have, and I may not be sitting in London writing this post. Most people do not plan their finances, they don’t think about inflation, don’t understand the power of compounding, and may regret this later in their lives.

Several potential investors ask me why I’m focusing on retail investors a.k.a the “lost cause” at CityFALCON . Why not just focus on the big banks, hedge funds and institutions!? Imagine how many lives you can change by helping average people generate higher than inflation returns.

WATCH OUT FOR INFLATION

Most of you seem to be worried about your money lying idle in the bank, earning not-worth-talking-about interest rates, but do not seem to be able to do much about it. You could blame your busy lifestyle or lack of finance knowledge, but you may be compromising your future by NOT managing your savings today.

Inflation is a complicated topic, is affected by several factors, and will differ from country to country. Please feel free to share your feedback or experiences in the comments section at the bottom of this page.

HOW INFLATION EATS YOUR PIE

Over a period of time, prices for products and services that we consume, rise. If your money does not grow at the same rate, the value of your wealth goes down. You may not feel the real impact of this if you have steady income coming in each month, but imagine what happens when you retire.

For instance, if you have $100 in your bank account, and your transport costs $10 per year, you can afford to pay for 10 years of transport. However, if cost of transport goes up by 10% each year to $11, $12, $13, and so on, your $100 will be over only in 8 years.

IS LOOKING JUST AT INFLATION ENOUGH?

What gets included in an inflation measure and the weightages of items in there differ from country to country, and your consumption and lifestyle may be completely different from averages considered in these measures. Discretionary spend such as holidays, dining out, etc is generally not included, and hence the ‘real inflation for you’ may be much higher than the reported one.

CASE IN POINT – INDIA

What happened in India over the last 2 decades should help you understand why looking at just the ‘reported’ inflation figure may not be good enough. People in other emerging markets could relate to this, but please remember that every market is different.

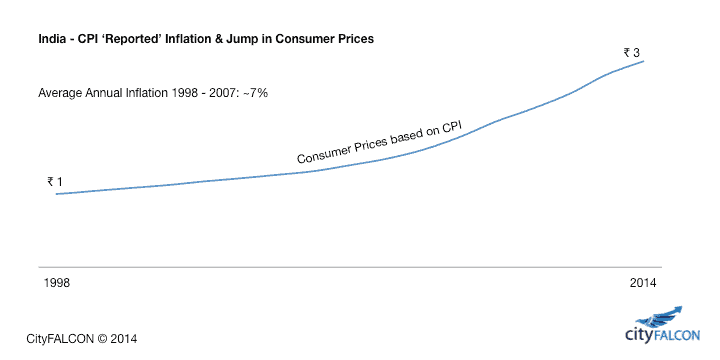

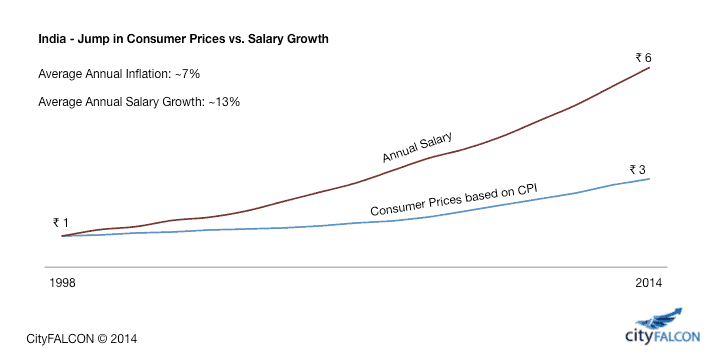

The chart below shows that a basket of goods and services that costed ₹ 1 in 1998, now costs ₹ 3 in 2014 based on reported inflation figures.

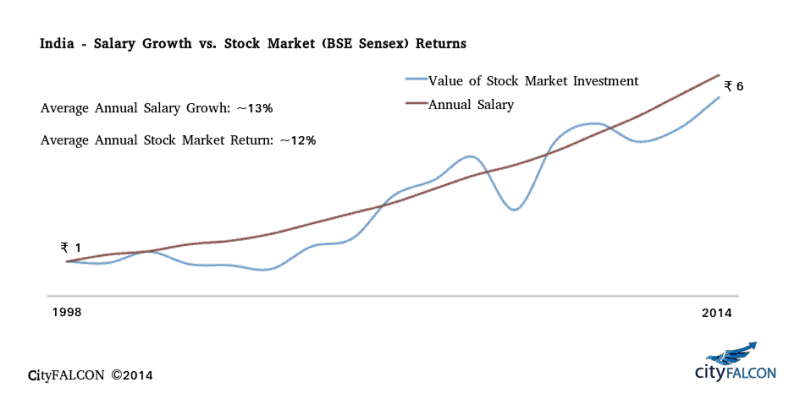

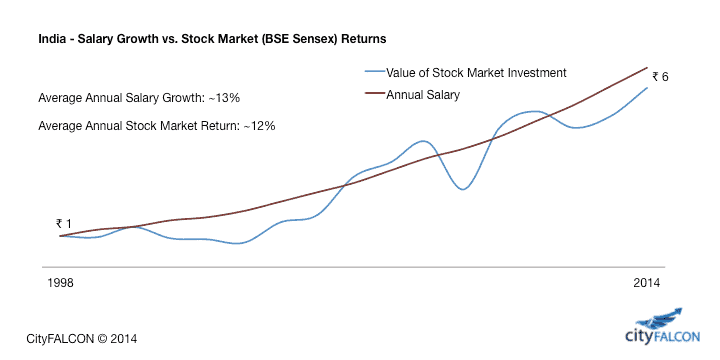

However, when you plot salary growth alongside consumer prices in the same chart, you can see much higher than inflation growth in salaries due to economic boom in the country. A person earning ₹ 1 in 1998, now earns ₹ 6. He or she is likely to increase their discretionary spending including on travel, house and car purchases, dining out, etc., thereby driving up the prices of these products and services. This means that the real inflation for you to consider is much higher. So, if you had retired before this economic boom, could you today afford to dine out or travel?

If you were ready to take some risk and had invested in the stock market, you could have also taken advantage of the economic boom which led to this level of salary growth. An investment of ₹ 1 in stock market in 1998 would now be ₹ 6, which would allow you to maintain your lifestyle even if you are no longer working.

CONCLUSION

We are not recommending that you invest in the stock market, but just that you need to start thinking about your money and your future.

WHAT’S NEXT?

Leave a Reply